-

-

My Account

Protect and Provide: How You Could Save Your Church Thousands with Workers' Comp

Whether your church employs 50 people across several campuses or 3 people in a single location, injuries on the job can happen to anyone. Your janitor might fall off a ladder while changing a lightbulb, or your pastor might trip and fall down the stairs after a Sunday service. When these accidents happen, you will want to have a system in place to care for an employee’s needs and cover the cost of unexpected medical bills.

“In most states, workers’ compensation is required for most employers. But even if your organization is exempt from purchasing workers’ compensation coverage according to your state laws, it’s beneficial to have the coverage as a way to provide for your employees,” said Pam Moore, a workers’ compensation premium audit manager at Brotherhood Mutual Insurance Company. “It also protects you from the financial ramifications of lawsuits relating to on-the-job injuries.”

Why is workers’ compensation coverage important for churches?

Workers' compensation laws ensure payment of medical bills for an employee injured on the job without the employee needing to sue. If an injury or illness occurs due to an accident within the scope of someone’s job, health insurance may not cover treatment costs. Instead, workers’ compensation can pay for those and other related costs, regardless of fault.

“Employers are responsible for medical, disability, rehabilitation, and death benefits when an employee is injured in work-related activities,” said Moore. "Those costs can add up quickly and create significant financial burden for ministries. Having workers' compensation coverage protects ministries by transferring the financial risk of these expenses to the insurance company."

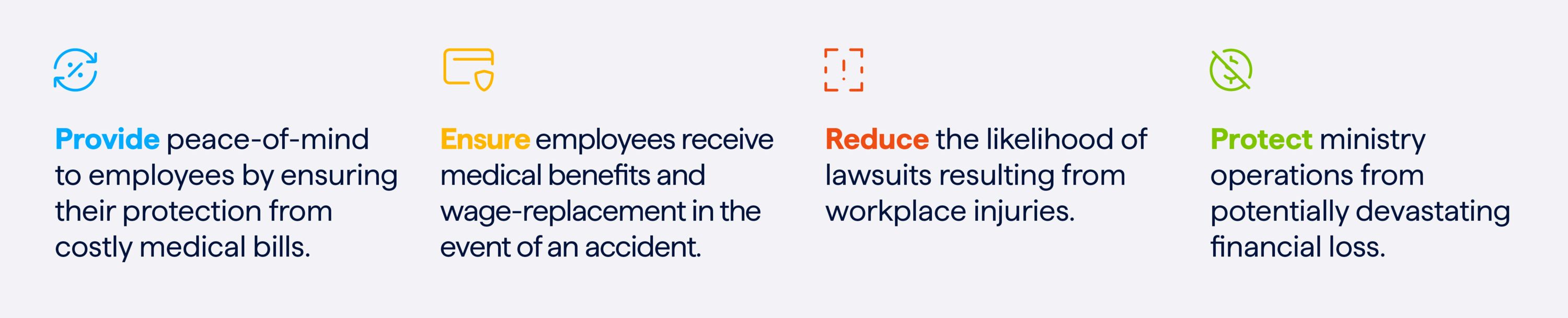

Purchasing workers’ compensation coverage is a proactive way for ministries to ensure their work and mission continue, even in the wake of a work-related accident. With workers’ compensation, ministries can:

- Provide peace-of-mind to employees by ensuring their protection from costly medical bills.

- Ensure employees receive medical benefits and wage-replacement in the event of work-related accidents.

- Reduce the likelihood of lawsuits resulting from workplace injuries.

- Ensure ministry can continue without potentially devastating financial loss.

What does workers’ compensation cover?

There are four types of disability benefits workers’ compensation can provide for employees who are injured when working on behalf of their employer.

- Temporary Total Disability (TTD): Employee is expected to recover and is currently incapacitated.

- Temporary Partial Disability (TPD): Employee is expected to recover and is partially incapacitated. The employee may be able to return to light duty work or shorter hours.

- Permanent Total Disability (PTD): Employee is not expected to recover. This benefit is for an injury that has rendered the employee fully incapacitated for life.

- Permanent Partial Disability (PPD): Employee is not expected to fully recover.

When you have workers’ compensation coverage, the benefits above apply to both part-time and full-time employees, but not to true independent contractors or volunteers. Ask your agent about other policies that cover the injuries of people who are not employed by your church.

What church leaders should know about workers’ compensation

Because workers’ compensation policies depend on employees and the scope of their roles, it can be confusing to determine what your church needs. Consider these common questions to help inform your decisions about workers’ compensation.

What does my state say about workers’ compensation?

Most states require all businesses, including ministries, to have some form of workers’ compensation coverage. These requirements vary by state, with some states requiring the coverage to be purchased through a state program, some requiring companies to purchase it through private insurance company programs, and others allowing a mix of the two options. No two states are the same, so it is important to talk to your agent about the expectations in your state.*

If my state doesn’t require me to have workers’ compensation coverage, do I still need it?

If your number of employees is below a certain threshold, your state might not require you to provide workers’ compensation coverage — but it is still a good idea to have a policy.

“Sometimes people don’t realize how important a workers’ compensation policy is,” said Jason Rochester, an agent and sales producer for American Church Group of South Carolina. “A church might have two people on staff — a pastor and a secretary — and everyone else is a volunteer. But those two paid employees play a critical role within the ministry, and if something happens to one of them while they’re at work, the liability may fall on the church. We once worked with a church whose pastor mowed the lawn as part of his role. One weekend, the lawn mower fell on the pastor and broke his leg. Because they didn’t have workers’ compensation coverage, the church had to find the money to pay for all those medical bills.”

It may be easy to overlook workers’ compensation if it isn’t a requirement, especially because roles within a church may not be considered dangerous. But Rochester cautioned against opting out of the coverage. “You can’t guarantee that someone won’t get hurt on the job,” he said. “If an accident happens, you should be confident that you have the coverage to provide for your employee’s needs and protect against liability.”

Can I choose which employees to include on my workers’ compensation policy?

Rochester said he often hears questions about getting coverage for only full-time employees or for certain people depending on their roles.

“Typically, all full-time and part-time employees must be included on your workers’ compensation policy,” said Rochester. “Some people think it might be easier to save some money on the policy by only getting coverage for a few people — but this is an all-or-nothing coverage, and it’s often more cost-effective to have it. Even if you could exclude someone, you might end up regretting it if that person experiences an injury or illness related to their work.”

How is my premium for workers’ compensation coverage determined?

Most workers’ compensation premiums depend on payroll data like estimated figures and the classification of your employees. Each role has a code that corresponds to a certain rate based on level of risk. Insurance companies are often required to audit the payroll data of workers’ compensation customers to ensure that the numbers estimated at the beginning of the year are reconciled with the actual payroll from the year.

“When we work with ministry customers who already have workers’ compensation coverage, we make sure to go over their employees, the roles they fill, and their estimated payment in those positions,” said Rochester. “Otherwise, we might find out that their payroll doesn’t match the remuneration provided on their workers’ compensation policy. I always want to sit down and talk through all the details with customers and prospects; I don’t want to make assumptions that could leave them vulnerable to over- or underpaying. Then, once they have a policy that meets their needs, the insurance company audits any changes annually to make sure everything lines up.”

Bonus Tip: You can get workers' compensation coverage based on actual payroll data rather than estimates with a streamlined audit. Learn more here.

Do I need to report injuries my employees sustain even if they’re minor?

Yes. States often mandate reporting and documentation any time an employee is injured on the job — even if the employee refuses medical care. If a report is made too late, a fine may be issued for the delay. Talk to your agent about what is required in your state, and check your state workers’ compensation website for the required forms.

What to ask your agent about workers’ compensation

Next time you talk to your agent, consider asking some of these questions to ensure your church has the workers’ compensation coverage you need.

- What are the workers’ compensation requirements in my state?

- Who in my organization will be covered by workers’ compensation if they are injured while working on behalf of the organization?

(Tip: Bring a list of anyone who works for your ministry in any capacity to help your conversation.) - What other policies might I need to protect volunteers if they are injured while working on behalf of our organization? What about independent contractors?

- How does workers’ compensation interact with other coverages such as health benefits? Do multiple policies pay on the same injury? What pays first?

- We have missionaries on staff; do they need a different type of workers’ compensation when they travel to other countries?

- Would my ministry benefit from a risk management review with an agent to identify exposures we might be overlooking?

A workers’ compensation policy can offer protection for both your church and the employees who carry out your mission every day. Ensuring sufficient coverage allows you to serve your community with confidence, knowing your staff will be well supported and your finances will be protected in the event of a work-related injury.

*Note: Brotherhood Mutual Workers’ Compensation insurance is not available in North Dakota, Ohio, Washington, and Wyoming. These states require employers to buy workers’ compensation insurance through a monopolistic state fund.

Additional Resources

- Workplace Injury Prevention

- Missionaries and Workers' Comp

- Use Caution When Classifying Workers

- Construction: Using Volunteer Workers

- Legal Assist FAQ: Does workers' compensation cover independent contractors?

- Legal Assist FAQ: Could we owe taxes or workers' comp benefits in connection with independent contractors?

Posted February 2024

The information provided in this article is intended to be helpful, but it does not constitute legal advice and is not a substitute for the advice from a licensed attorney in your area. We strongly encourage you to regularly consult with a local attorney as part of your risk management program.

Request A Quote

Thank you for your interest in Brotherhood Mutual. We appreciate the opportunity to provide your church or other ministry with an insurance quote and will reply to your request as soon as possible.

Submit Your Question

Text to follow...